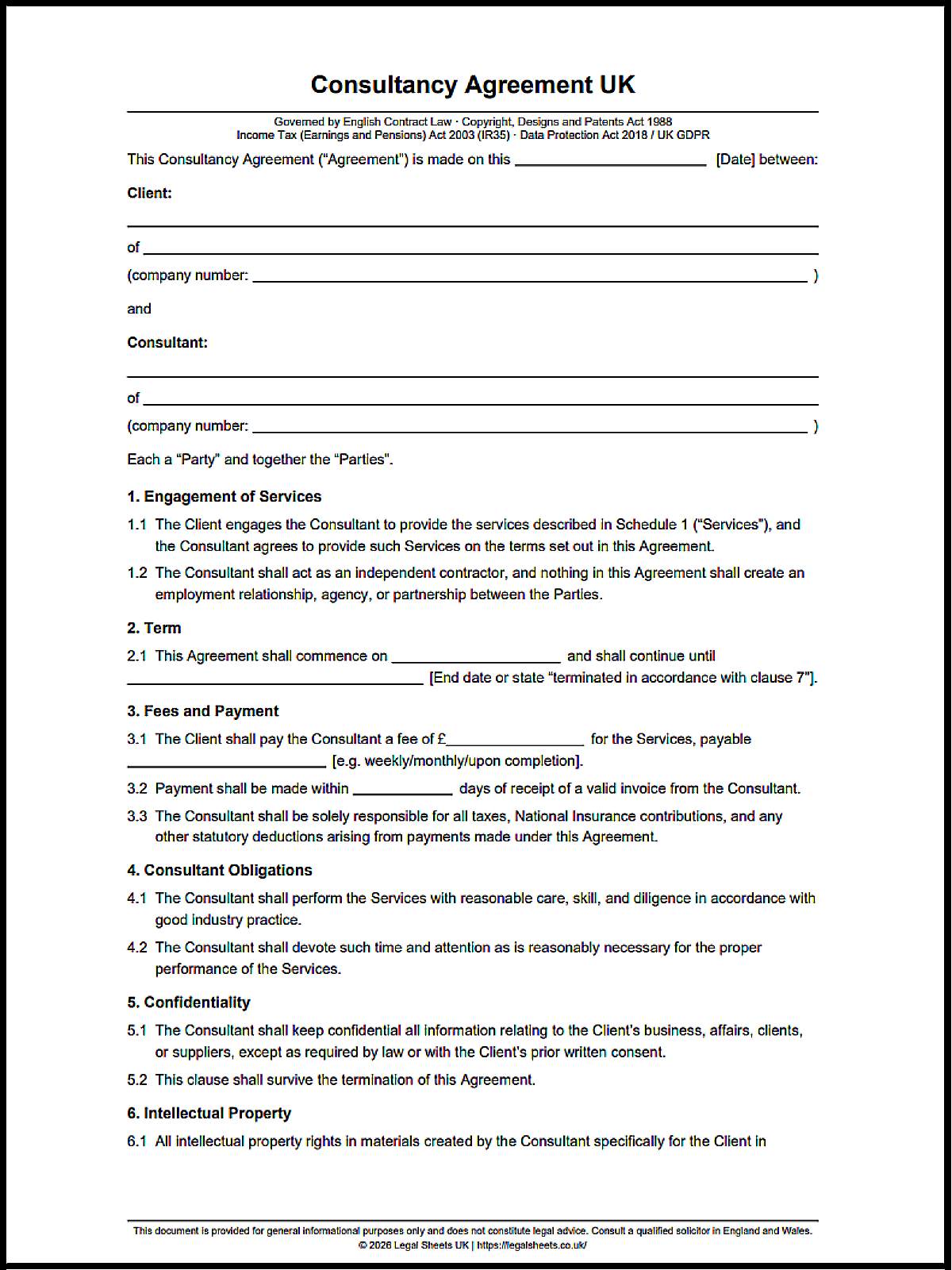

Consultancy Agreement Template (PDF & Printable Formats)

Many people searching for a Consultancy Agreement are doing so after a project has already expanded beyond what was originally discussed, with disagreements emerging over fees, deadlines, or the work that was actually expected. In England, a poorly drafted consultancy contract can create significant problems when payment is withheld or a consultant claims additional work falls outside the agreed scope, even where the arrangement appears straightforward.

The issue often surfaces in county court proceedings where judges are asked to interpret scattered emails and informal instructions because the written agreement never properly defined deliverables, ownership of work product, or termination rights. Companies engaging consultants should also consider execution requirements under the Companies Act 2006, particularly where the agreement is signed on behalf of a company.

The template and accompanying guidance here are designed to support a clear commercial arrangement before those disputes arise.

Consultancy Agreement Template (PDF, Word & Printable Formats)

Why Businesses Put Consultancy Agreements in Place Before Work Starts

Most consultancy disputes originate from assumptions made at the beginning of the relationship.

Preventing Employment Status and IR35 Problems

Many businesses focus on commercial terms and overlook status issues until HMRC raises questions or a consultant asserts statutory rights.

Avoiding Disguised Employment Risks

Contractual wording alone does not determine status. Working practices remain highly influential.

Establishing Independent Contractor Status

Clear documentation assists in demonstrating the parties’ intended commercial relationship.

Separating Project Outcomes from Employee-Style Supervision

A consultant is usually engaged to deliver outcomes rather than operate under employee-style management structures.

Reducing Future Tax Disputes

Ambiguity around status frequently becomes expensive when examined retrospectively.

Avoiding Commercial Disputes Before They Arise

Most litigation stems from uncertainty rather than deliberate wrongdoing.

Defining the Scope of Services

A clear scope reduces disagreements about what work is included within the agreed fee.

Clarifying Payment Expectations

Payment disputes become significantly harder to resolve when billing arrangements are vague.

Setting Ownership of Work Product

Clients often assume ownership transfers automatically. Under the verified legal framework, intellectual property created by an independent consultant does not automatically vest in the client.

Protecting Confidential Information

Confidentiality obligations become particularly valuable when commercially sensitive information is shared throughout the project.

Protecting Both Parties if the Relationship Ends Early

Not every consultancy project reaches its intended conclusion.

Notice Requirements

Termination provisions establish how the relationship can be brought to an orderly close.

Payment Obligations

Outstanding invoices and accrued fees should be addressed clearly.

Return of Company Information

Businesses frequently require return or deletion of confidential materials.

Handover of Completed Work

Project continuity often depends upon proper transfer of completed deliverables.

Decisions That Should Be Made Before Drafting the Consultancy Contract

Many drafting problems originate because commercial decisions have not been made before documentation begins.

Defining the Services Being Purchased

The more specific the service description, the easier it becomes to manage expectations and performance.

Specific Deliverables

Deliverables should be identified with enough precision that both parties understand what constitutes completion.

Advisory Versus Operational Responsibilities

Consultants engaged to provide advice face different expectations from those delivering operational services.

Milestones and Deadlines

Projects with multiple stages benefit from documented milestones.

Acceptance Criteria

Acceptance mechanisms reduce arguments over whether deliverables satisfy contractual requirements.

Choosing How the Consultant Will Be Paid

Fee structures influence both commercial expectations and project management.

Fixed-Fee Arrangements

Suitable where deliverables are clearly defined.

Daily-Rate Engagements

Common where workload cannot be predicted precisely.

Hourly Billing Structures

Often used for advisory and support services.

Retainer Agreements with commission payments

Useful where ongoing access to expertise is required.

Expenses and Reimbursements

Disputes frequently arise when expense approval procedures are not documented.

Determining Ownership of Intellectual Property

One of the most expensive assumptions in consultancy engagements is that ownership transfers automatically.

Reports and Documentation

Ownership should be addressed expressly.

Software and Code

Technology projects require particular attention.

Designs and Creative Works

Creative outputs frequently carry significant commercial value.

Research and Methodologies

The agreement should distinguish between project deliverables and pre-existing materials owned by the consultant.

Clauses That Have the Greatest Impact During a Consultancy Relationship

Many consultancy agreements contain dozens of provisions, but only a handful regularly become central during disputes. These are usually the clauses that determine payment entitlement, ownership of work, confidentiality obligations, liability allocation, and the circumstances in which the engagement can be brought to an end.

Scope of Services Clause

Scope disputes are among the most common causes of commercial disagreement. A consultant may believe a task falls outside the agreed engagement, while the client may view it as part of the original instruction.

Defining Responsibilities Clearly

The agreement should identify precisely what services will be provided. Broad descriptions often create uncertainty when project expectations expand.

Managing Scope Creep

Projects frequently evolve after commencement. Without a mechanism for approving additional work, consultants may find themselves performing substantial extra services without corresponding fee increases.

Handling Additional Work Requests

A structured variation procedure can reduce disagreements by documenting changes before additional work begins.

Fees, Invoicing and Payment Terms

Payment clauses often receive limited attention during drafting but become critically important when relationships deteriorate.

Invoice Schedules

Regular billing schedules create predictability for both parties and reduce disputes regarding when payment becomes due.

Late Payment Provisions

Late payment disputes can quickly damage a commercial relationship. Clear contractual provisions establish expectations from the outset.

Payment Disputes

Businesses often challenge invoices where deliverables have not been clearly defined or where scope changes were agreed informally.

VAT Considerations

Consultants operating through registered businesses should ensure VAT treatment aligns with their commercial and regulatory obligations.

Confidentiality Obligations

Confidentiality clauses are often relied upon long after the consultancy engagement has ended.

Commercially Sensitive Information

Business plans, pricing structures, internal processes, and strategic information frequently require protection.

Trade Secrets

The value of consultancy services often depends on access to confidential operational information. A breach may create commercial damage that continues long after termination.

Client Data

Where confidential information includes personal data, separate data protection obligations may also apply.

Continuing Obligations After Termination

Confidentiality responsibilities commonly survive termination because commercial sensitivity rarely ends when the project concludes.

Intellectual Property Assignment Clauses

Intellectual property ownership regularly becomes a significant issue only after a project succeeds commercially.

Present Assignment Wording

Under the verified legal framework, intellectual property created by an independent consultant does not automatically transfer to the client. Section 90 of the Copyright, Designs and Patents Act 1988, Section 90 requires assignment arrangements to be in writing and signed by or on behalf of the assignor.

More information can be found within the official legislation: Copyright, Designs and Patents Act 1988, Section 90.

Future Copyright Ownership

One recurring drafting mistake involves language stating that the consultant will assign intellectual property at a future date. The verified legal facts identify this as a significant ownership risk because a promise to assign may not transfer legal title immediately.

Ownership of Deliverables

Ownership provisions should identify precisely which deliverables transfer and whether any pre-existing consultant materials remain excluded.

Protection Against Later Ownership Disputes

Projects involving software, research materials, technical documentation, or valuable commercial content particularly benefit from robust ownership drafting.

Liability and Indemnity Provisions

Commercial relationships involve risk allocation as much as service delivery.

Financial Risk Allocation

Liability clauses determine how losses are distributed if something goes wrong.

Professional Negligence Exposure

Consultants providing specialist advice may face substantial exposure where clients rely on recommendations during significant commercial decisions.

Limitation of Liability Clauses

Many parties negotiate liability caps to create greater certainty regarding potential financial exposure.

Insurance Requirements

Professional indemnity insurance requirements are often included where the engagement involves material commercial risk.

Termination and Exit Provisions

Even successful projects eventually conclude.

Immediate Termination Events

Serious breaches commonly trigger immediate termination rights.

Notice-Based Termination

Many consultancy arrangements permit termination upon a specified notice period.

Outstanding Payments

The agreement should address how unpaid fees will be treated after termination.

Return of Materials and Information

Businesses frequently focus on the return of confidential information, company property, and project documentation once the engagement ends.

Managing IR35 Risk Throughout the Consultancy Engagement

IR35 concerns often arise long after the contract has been signed. Businesses frequently assume the written agreement determines status, only to discover that HMRC and tribunals examine how the relationship actually operated in practice.

Why Contract Wording Alone Does Not Determine Status

The verified legal framework makes clear that contractual labels do not automatically determine status outcomes.

Actual Working Practices

Courts and tribunals examine how the parties behaved during the engagement rather than relying solely on written declarations.

Degree of Control

A consultant subject to extensive supervision, mandatory procedures, and employee-style management may face greater status scrutiny.

Integration into the Client Business

The more integrated a consultant becomes within internal structures, the more difficult it may be to support independent contractor treatment.

Independence in Day-to-Day Operations

Operational independence often carries significant weight when status is examined.

Status Determination Statement (SDS) Requirements

The Status Determination Statement is one of the most significant compliance obligations within the off-payroll working regime.

When an SDS Is Required

Under the verified legal facts, medium and large end-clients are required to assess status and issue a Status Determination Statement before payments begin.

Further information is available through the official legislation: Income Tax (Earnings and Pensions) Act 2003.

Who Must Issue It

Responsibility generally falls on qualifying end-clients rather than the consultant.

Information That Should Be Included

The SDS must state whether the engagement is considered inside or outside IR35 and provide reasons supporting that conclusion.

Timing Requirements Before Payment

Failure to deal with status obligations before payments commence can produce significant tax consequences.

Small Company Exemption Considerations

Not every client carries the same obligations.

Statutory Size Thresholds

According to the verified legal facts, a company generally qualifies for the exemption only if it satisfies at least two of the following criteria:

| Threshold Category | Requirement |

|---|---|

| Annual turnover | Not exceeding £15 million |

| Balance sheet total | Not exceeding £7.5 million |

| Employees | Not exceeding 50 employees |

Common Mistakes When Relying on Exemptions

Businesses sometimes rely on outdated thresholds and incorrectly conclude that exemption status applies after shareholder changes.

Consequences of Incorrect Assessments

Where exemption assumptions prove incorrect, the financial consequences may extend to backdated tax liabilities, interest, and penalties.

Challenging an SDS Decision

Status assessments are not always accepted without challenge.

Consultant Disagreement Process

The verified legal framework provides a formal disagreement process where a consultant contests the determination.

The Client’s 45-Day Response Obligation

A client receiving an objection must respond within 45 days by either maintaining the original assessment with reasons or issuing a revised determination.

Liability Consequences for Failing to Respond

Failure to meet the statutory response requirement may shift tax liabilities to the client.

Data Protection Issues Often Overlooked in Consultancy Agreements

Data protection obligations frequently receive attention only after a security incident occurs. By that stage, contractual deficiencies may already have created regulatory exposure.

When Article 28 Clauses Become Mandatory

The verified legal facts identify circumstances where contractual processor provisions are required.

Consultants Acting as Data Processors

Where a consultant processes personal data on behalf of the client, mandatory contractual obligations arise.

Access to Customer Information

Customer databases, support records, and marketing systems often involve personal data processing activities.

Access to Employee Records

HR-related consultancy projects commonly involve access to employee information.

Outsourced Operational Services

Operational support services frequently involve ongoing processing of personal data.

Data Processing Obligations That Must Be Covered

Article 28 requires specific contractual content.

Processing Instructions

Consultants must process personal data only in accordance with documented instructions.

Confidentiality Requirements

Individuals handling data must remain subject to confidentiality obligations.

Security Measures

Appropriate technical and organisational safeguards must be addressed.

Sub-Processor Controls

The verified legal framework requires prior authorisation before appointing sub-processors.

Data Deletion or Return Obligations

The agreement should address what happens to personal data once the engagement ends.

Additional guidance is available from the official regulator: Information Commissioner’s Office (ICO).

Risks of Missing Data Protection Terms

Contractual omissions can create consequences even where no breach occurs.

ICO Investigations

Regulatory scrutiny may focus on contractual compliance as well as operational conduct.

Regulatory Penalties

The verified legal facts identify potential exposure to administrative fines.

Contractual Compliance Failures

Non-compliant processor arrangements may place both parties in breach of statutory requirements.

Increased Liability Following Data Breaches

Weak contractual provisions frequently become a significant issue after a security incident has already occurred.

Intellectual Property Problems That Commonly Surface After the Project Ends

Ownership disputes often emerge only after work becomes commercially valuable.

Why Ownership Does Not Automatically Transfer to the Client

Many businesses incorrectly assume payment automatically transfers ownership rights.

Independent Contractor Ownership Rules

The verified legal framework confirms that intellectual property created by an independent consultant does not automatically vest in the client.

Written Assignment Requirements

Ownership transfer requires written assignment signed by or on behalf of the consultant.

Risks of Relying on Informal Agreements

Informal understandings frequently become difficult to enforce when commercial relationships deteriorate.

Drafting Mistakes That Create Ownership Disputes

Certain drafting errors appear repeatedly in consultancy disputes.

Future Promises to Assign IP

Promises to transfer ownership later may fail to provide immediate legal title.

Missing Assignment Language

Incomplete ownership provisions can leave valuable rights with the consultant.

Unclear Ownership of Project Materials

Reports, designs, software, databases, and supporting materials should all be addressed expressly.

Protecting Commercial Rights After Completion

Successful projects often depend upon certainty regarding ownership.

Ownership Confirmations

Confirmation provisions reduce uncertainty once deliverables have been completed.

Further Assurance Provisions

These clauses may require additional documents to perfect ownership transfers if necessary.

Transfer of Supporting Materials

Ownership disputes frequently extend beyond the main deliverable to supporting files, documentation, and related materials.

Restrictive Covenants and Post-Termination Restrictions

Businesses frequently try to protect customer relationships and commercially sensitive information after a consultancy engagement ends. The difficulty is that restrictions which appear reasonable during drafting can become unenforceable when tested in court.

Restrictions Courts Commonly Scrutinise

English courts examine post-termination restrictions carefully, particularly where they interfere with a consultant’s ability to earn a living.

Non-Compete Clauses

Restrictions preventing a consultant from working for competitors are often challenged when they extend beyond what is genuinely necessary to protect legitimate business interests.

Non-Solicitation Provisions

Clients commonly seek to prevent consultants from actively approaching customers, suppliers, or employees through affiliate programmes after the engagement ends.

Non-Dealing Restrictions

These provisions go further by restricting dealings even where the client initiates contact.

Industry-Wide Prohibitions

Broad restrictions covering entire sectors frequently attract scrutiny because they may go beyond what is necessary to protect confidential information or goodwill.

When Post-Termination Restrictions Become Unenforceable

The verified legal framework notes that restrictive covenants are assessed under the doctrine of restraint of trade.

Excessive Duration

Long restrictions often become difficult to justify, particularly where confidential information loses commercial value over time.

Overly Broad Geographic Scope

Geographic restrictions should reflect the actual commercial reach of the business rather than theoretical markets.

Lack of Legitimate Business Interest

Courts are unlikely to enforce restrictions that appear designed merely to eliminate competition.

Alternative Ways to Protect Commercial Interests

Many businesses achieve stronger protection through focused contractual drafting rather than broad restrictive covenants.

Confidentiality Obligations

Confidentiality provisions often remain the most reliable method of protecting sensitive information.

Intellectual Property Protections

Clear ownership provisions can prevent disputes over commercially valuable deliverables.

Client Relationship Safeguards

Targeted restrictions focused on specific customer relationships may be easier to justify than broad market-wide prohibitions.

Common Consultancy Agreement Failures That Lead to Disputes

Most consultancy litigation originates from a relatively small number of recurring mistakes. The same drafting and operational failures appear repeatedly in tribunal claims, tax investigations, and commercial disputes.

Treating a Consultant Like an Employee

The most expensive consultancy disputes often begin long before any legal proceedings arise.

Worker Status Claims

The verified legal framework highlights that courts and tribunals examine operational reality rather than contractual labels.

Employment Tribunal Risks

A consultant who successfully establishes worker or employee status may pursue statutory rights despite contractual wording describing them as self-employed.

Backdated Employment Rights

Status reclassification can create exposure relating to holiday pay, minimum wage obligations, pension issues, and other statutory rights.

Using Generic Online Consultancy Contracts

Many disputes originate because businesses download generic documents without adapting them to the engagement.

Missing Industry-Specific Provisions

Technology, compliance, healthcare, and regulated-sector projects often require more detailed contractual protections.

Weak IP Protection

Ownership provisions copied from generic templates frequently fail to reflect the requirements of the Copyright, Designs and Patents Act 1988.

Inadequate Compliance Clauses

Data protection obligations are commonly overlooked until regulatory concerns emerge.

Relying on Outdated IR35 Assumptions

IR35 rules continue to create significant compliance challenges.

Incorrect Company Size Assessments

The verified legal framework identifies reliance on outdated small-company thresholds as a recurring compliance failure.

Missing SDS Obligations

Where a Status Determination Statement should have been issued but was not, the consequences can extend beyond administrative inconvenience.

HMRC Exposure

HMRC assessments may involve substantial financial liabilities, particularly where engagements have operated for extended periods.

Assuming Tax Indemnities Always Solve IR35 Problems

Many businesses place significant reliance on tax indemnity provisions.

Enforcement Difficulties

A contractual indemnity is only as valuable as the financial position of the party expected to honour it.

PSC Insolvency Risks

The verified legal framework notes that consultants operating through Personal Service Companies may cease trading, leaving limited recovery options.

Commercial Recovery Challenges

Recovering substantial liabilities through litigation can prove difficult even where contractual rights exist on paper.

Consultancy Agreement Compared With Similar Business Documents

Confusion between related business documents regularly creates drafting problems. Each document serves a different commercial purpose.

Consultancy Agreement vs Employment Contract

The distinction matters because different legal consequences may follow.

Nature of the Working Relationship

An employment contract creates an employment relationship. A consultancy agreement is intended to document an independent business-to-business engagement.

Tax Treatment

The verified legal framework highlights the significance of status assessments and IR35 considerations in consultancy arrangements.

Employment Rights Implications

Employment contracts carry statutory employment protections that may not apply to genuine consultancy relationships.

Consultancy Agreement vs Freelancer Agreement

The terminology is sometimes used interchangeably, but practical differences often exist.

Scope and Complexity Differences

Consultancy agreements frequently involve broader commercial protections, confidentiality obligations, intellectual property provisions, and liability clauses.

Corporate Consultancy Engagements

Corporate clients often require more extensive contractual protections than those typically seen in simpler freelance engagements.

Commercial Risk Allocation

Risk allocation provisions are usually more detailed in consultancy agreements involving substantial commercial projects.

Consultancy Agreement vs Statement of Work

These documents often operate together rather than replacing one another.

Framework Agreement Versus Project Specification

The consultancy agreement establishes the overall contractual relationship, while a statement of work commonly addresses project-specific deliverables and milestones.

How Both Documents Operate Together

Businesses frequently use a master consultancy agreement supported by multiple project-specific statements of work.

Consultancy Agreement vs Agency Contractor Arrangement

Agency structures introduce additional parties and responsibilities.

Supply Chain Responsibilities

Contractual obligations may be distributed across the consultant, agency, and end-client.

Status Determination Obligations

IR35 responsibilities can become more complex where agencies participate in the engagement structure.

Payment Structures

Agency arrangements often involve separate invoicing and payment chains.

Using the Consultancy Agreement During the Engagement

Signing the contract is only the beginning. Day-to-day conduct often determines whether the agreement functions effectively when disputes arise.

Onboarding the Consultant

The onboarding process frequently shapes how the relationship operates throughout the engagement.

Access Permissions

Access should be limited to systems genuinely required for the consultant’s work.

Information Sharing

Businesses should ensure commercially sensitive information is disclosed only where necessary.

Compliance Requirements

Consultants may need to comply with internal policies relating to confidentiality, security, and data protection.

Managing Performance Without Creating Employment Indicators

Many businesses unintentionally undermine consultancy arrangements through operational practices.

Outcome-Based Supervision

Focusing on deliverables rather than day-to-day control may better reflect an independent contractor relationship.

Project Reporting

Progress reporting can be structured around milestones and outcomes rather than employee-style supervision.

Deliverable Reviews

Reviewing completed work generally presents fewer status concerns than directing every aspect of how services are performed.

Handling Changes During the Project

Few consultancy projects remain static.

Scope Amendments

Changes should be documented before additional work begins.

Fee Adjustments

Fee revisions are easier to enforce when recorded clearly.

Additional Services

New services often require revised commercial and operational terms.

Bringing the Consultancy Relationship to a Close

The final stage of the engagement is often overlooked during planning.

Final Deliverables

Completion requirements should be verified before final payment.

Data Return Requirements

The verified legal framework identifies data deletion and return obligations as important compliance considerations where personal data has been processed.

IP Transfer Confirmation

Businesses commonly seek written confirmation that ownership provisions have been implemented correctly.

Final Invoices

Outstanding financial obligations should be resolved before the parties disengage completely.

UK Legal Facts and Compliance Requirements

Legal Requirements

| Topic / Issue | England Legal Rule | Governing Law |

|---|---|---|

| Execution Formalities | Simple contracts may be signed physically or digitally. Deeds require statutory execution formalities and witnessing requirements. | Law of Property (Miscellaneous Provisions) Act 1989; Companies Act 2006 |

| IR35 Status Assessment | Medium and large clients must assess status and issue a Status Determination Statement before payment. | Income Tax (Earnings and Pensions) Act 2003, Part 2 Chapter 10 |

| Data Processing Obligations | Mandatory processor clauses apply where consultants process personal data on behalf of clients. | UK GDPR Article 28; Data Protection Act 2018 |

| Intellectual Property Vesting | Intellectual property created by consultants does not automatically transfer to clients. | Copyright, Designs and Patents Act 1988, Section 90 |

| Tax Evasion Facilitation | Businesses must not facilitate tax evasion through contractual or operational arrangements. | Criminal Finances Act 2017, Section 45 |

Practical Legal Impact

These rules influence consultancy agreements long after the document has been signed.

A missing Status Determination Statement can transfer tax liabilities to the client rather than the consultant. Weak intellectual property wording can leave ownership with the consultant despite full payment having been made. Missing Article 28 provisions may create regulatory compliance failures even where no personal data breach has occurred.

In practice, commercial disputes are commonly determined by the interaction between contractual wording and operational behaviour. A consultancy agreement that appears robust on paper may offer limited protection if working practices contradict its terms.

Where disputes involve status claims, Employment Tribunals examine the practical reality of the relationship. Purely commercial disputes such as unpaid invoices, confidentiality breaches, or ownership disagreements are generally dealt with through the County Court or High Court depending on the value and complexity of the claim.

Frequently Asked Questions

Can a Consultant Successfully Claim Worker or Employee Rights Even if the Contract Says They Are Self-Employed?

Yes. According to the verified legal framework, courts and tribunals may look beyond contractual labels and examine how the relationship operated in practice. If working arrangements resemble employment, status reclassification may occur despite self-employment wording.

What Happens if a Client Starts Paying a Consultant Before Issuing a Required Status Determination Statement?

The verified legal facts state that failure to comply with SDS requirements can result in tax liabilities transferring to the client. The consequences may include responsibility for PAYE deductions, National Insurance obligations, and related liabilities.

Further information can be found within the official legislation: Income Tax (Earnings and Pensions) Act 2003.

Does a Client Automatically Own Software, Reports, Designs or Other Work Created by a Consultant?

No. The verified legal framework confirms that intellectual property created by an independent consultant does not automatically vest in the client. Ownership transfer generally requires a written assignment signed by or on behalf of the consultant.

See: Copyright, Designs and Patents Act 1988, Section 90.

Can HMRC Ignore the Wording of a Consultancy Agreement During an IR35 Investigation?

HMRC may examine both the written contract and the actual working arrangements. The verified legal framework notes that contractual drafting alone does not determine status outcomes where operational reality points in a different direction.

Are Post-Termination Non-Compete Clauses in Consultancy Agreements Enforceable in Every Situation?

No. The verified legal facts indicate that post-termination restrictions are assessed under restraint of trade principles. Restrictions that are excessively broad or go beyond what is necessary to protect legitimate business interests may be declared unenforceable.